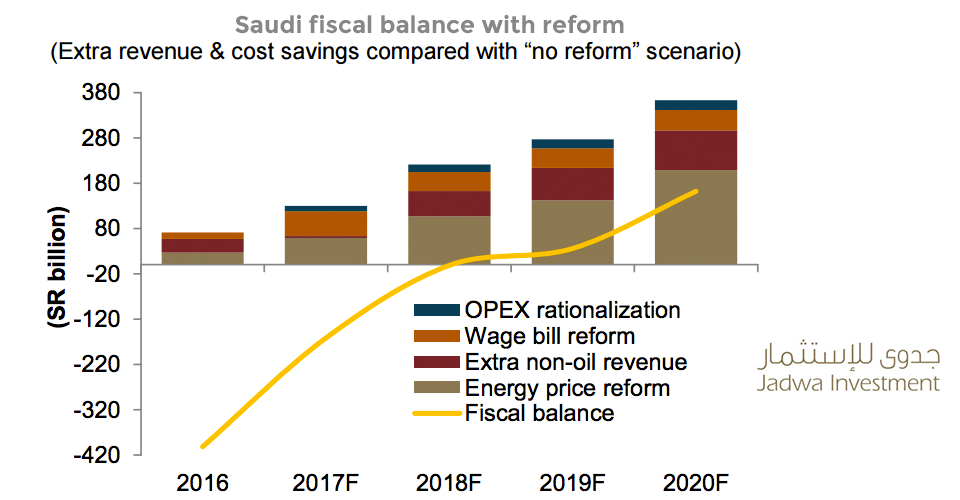

Fiscal reforms already underway in Saudi Arabia could save the Kingdom as much as SR362 billion ($97 billion) annually by 2020, leading to a surplus of SR162 billion ($43 billion) annually, according to a recent analysis by Jadwa Investment.

That amount is a significant increase as compared to if nothing was done to address Saudi Arabia’s fiscal situation. Without reforms, Saudi Arabia would have a fiscal deficit of SR200 billion ($53 billion) by 2020.

Deputy Crown Prince Mohammed Bin Salman.

The initiatives in place for the Kingdom to achieve fiscal balance by 2020 include roadmaps designated for enhancing spending efficiency, reforming energy prices, and promoting non-oil revenue – all part of the Fiscal Balance Program (FBP 2020) and Saudi Arabia’s Vision 2030 economic and social reform plan.

According to Jadwa Investment, the Kingdom has already begun its course-correction. The Riyadh-based bank said in a report that it estimates that FBP 2020 initiatives will result in SR100 billion ($26 billion) worth of gross savings in 2017 alone.

“The reduction in public sector worker allowances and wage freeze will contribute to 55 percent of 2017 gross savings. A further 29 percent of these savings will come from energy price reform – whilst new measures to enhance the efficiency of spending and raise non-oil revenue will contribute 12 percent and 4 percent, respectively. That being said, we believe that the government has already incorporated these savings into the 2017 budget, and therefore are confident of government delivering on reforms.”

[Click here to read the full report from Jadwa Investment on Saudi Arabia’s FPB 2020] [Arabic]